GM's Corner: Despite Extra Expenses, We’re Breaking Even in a Chaotic Year

by

Jon Roesser, Weavers Way General Manager

Working under the assumption that readers of the November Shuttle will want to read something – anything! – that’s not about politics, let’s take a dive into the Co-op’s financials. For those who struggle with sleep, read before bedtime.

After the end of our fiscal year (which ends June 30), we have an independent third-party auditor review the Co-op’s financials. This year’s audit was conducted in August and presented at the October meeting of the Co-op’s Board of Directors. The audit was unanimously approved by our board.

We received an unqualified opinion – a “clean” report – meaning the auditors found our financial statements fair and true. We’ve received a clean audit for at least the 12 years I’ve worked at the Co-op. Anything less would be unacceptable.

As for our FY2020, it can be summed up as such: Beginning July 1, 2019, 38 weeks of humdrum, followed by 14 weeks of bedlam. I yearn for humdrum.

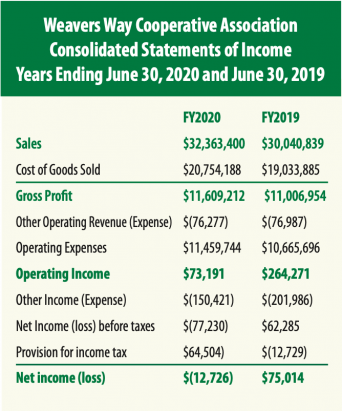

Sales were $32,363,400, 7.7% over prior year, a good number. Our gross profit (the money left over after paying our vendors for the products we sell) was $11,609,212, only 5.6% over prior year. Gross profit dollars are what we use to pay for the Co-op’s operations.

Why the gap between sales growth and gross profit growth? A substantial change in product mix in the fourth quarter (April-June) as high margin sales in prepared foods (things like hot bars and soup stations) collapsed while sales in low-margin packaged grocery and frozen foods skyrocketed.

So while 7.7% sales growth is good, the growth was disproportionately in lower margin departments.

Operating expenses grew at 7.4% over prior year, to $11,459,744. We incurred significant operating expenses in the fourth quarter related to the pandemic. Some of the bigger expenses we otherwise would not have had to contend with include the following:

- Battle Pay: $144,804

- Easter Holiday Pay: $9,508

- Extra “mental health” time off: $31,383.

- Sick pay for positive COVID cases and those needing to self-quarantine: $29,316.

One need not have gone to business school to know that when operating expenses rise at a faster pace than gross profits, net income will decline.

The bottom line: The Co-op lost $12,726 in FY2020. For a business with sales higher than $32 million, it’s essentially breaking even; COVID-related expenses were the difference.

For FY2021, which began July 1, the story is much the same. Sales have been strong, gross profits have been constricted by a disrupted sales mix, and higher-than-normal operating expenses are keeping us right around break-even. We may wind up making a little money in FY2021; we may wind up losing a little money.

In any case, the Co-op remains well-positioned to navigate through the stormy seas of the COVID pandemic.

Member equity grew $198,382 last fiscal year, to just under $2.2 million. Equity growth was significantly better than the prior year growth of $112,526, and the trend has continued into FY2021.

Our cash reserves increased by over $2.3 million last fiscal year. Like all smart businesses, the Co-op has taken steps to husband cash as we operate through not just the pandemic but also the accompanying economic downturn, which we expect will continue for the near term. For now, cash generated from operations is sufficient to meet our day-to-day obligations and pay down debt. Last month we paid off the last of our Chestnut Hill member loans and next month we’ll pay off the first round of our Ambler member loans.

For those of you who got this far, I will have more to present regarding the Co-op’s fiscal health at the General Membership Meeting, which will be virtual this year, on Thursday, Nov. 12. You can register to attend the meeting here.

You are also most welcome to send me suggestions, questions or comments: jroesser@weaversway.coop.

See you around the Co-op.